The S&P 500’s recent 10% decline has prompted many questions from investors about what this correction means for their portfolios. Though such downturns can naturally trigger concern, viewing these movements through a historical lens offers valuable context. In his latest article, “The Market has Corrected, What’s Ahead” Chris Fasciano, vice president, investment management and research, and chief market strategist, examines the factors behind the recent downturn, how similar events have played out in the past, and why maintaining a long-term focus remains key.

Zooming out from current volatility is also a useful exercise when exploring the current reality.

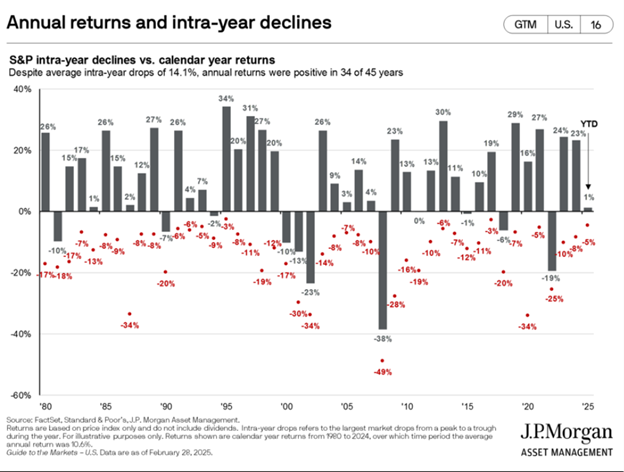

Despite negative headlines, not all parts of the market are struggling. While technology and consumer cyclical stocks – last year’s big winners – have led the recent decline, other sectors are holding up well. Consumer staples, health care and financial services have had stronger mid-single-digit returns. International stocks, as measured by the ACWI ex-USA Index are also up Year-to-date along with US Aggregate Bond Index also in positive return territory. In short, diversification is proving its value again after a long period where it didn’t seem to help as much. And, while market pullbacks never feel great, they do happen regularly, as shown in the JP Morgan Slide on Annual Returns and Intra-year declines as of 2/28/2025:

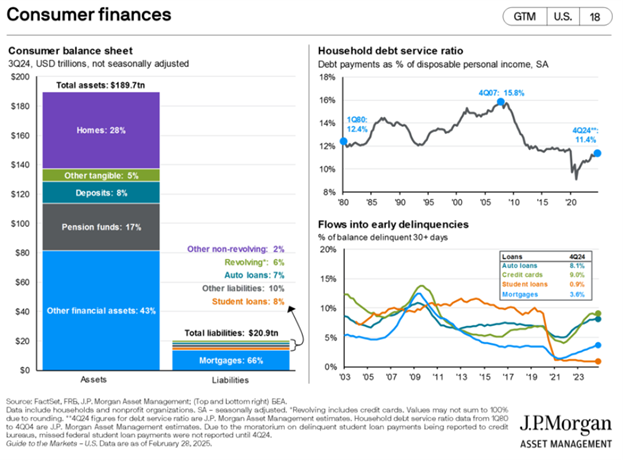

Additionally, when evaluating data to help us understand the current economic reality, it is useful to remember that we are a consumption-driven economy. With that in mind, it is then useful to look at the position of the consumer today, and in comparison, to historical timeframes. Below, the bar graph on the left shows current consumer assets to liabilities, and the top right chart below shows Household debt service ratio since 1980. While we often hear in the media of consumer debt delinquencies increasing at present (and that is illustrated in the bottom right chart for credit cards and auto loans), when we compare overall current household debt payments as a percentage of disposable personal income, we see current debt service ratio is quite low to averages going back to 1980. As such, this should lend to a level of longer-term resiliency around overall consumer consumption – even if presently we are seeing a slight slow-down in overall spending.

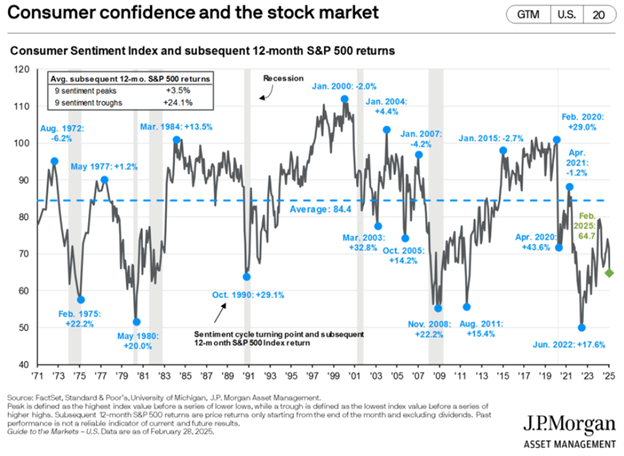

Another set of data that can be beneficial to look at over long time periods is Consumer Confidence and S&P 500 performance after peaks and troughs. Interestingly, troughs in sentiment tend to precede strong equity returns while peaks in sentiment do not see as much upside. This underscores that getting out of the market when sentiment is low can be a poor investment strategy.

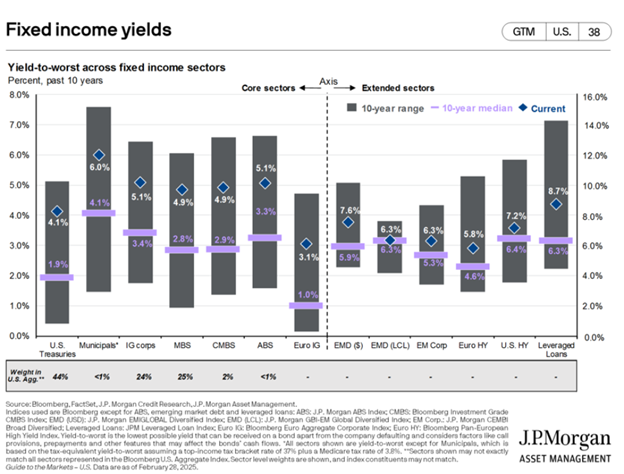

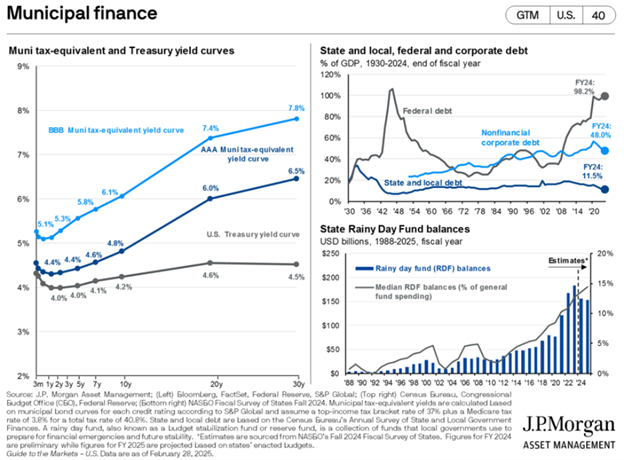

As we look forward, and consider deployment of capital available for investment, it is notable to look at fixed income yield-to-worst metrics across different areas of the bond market. What we see in the chart below is current yields are still elevated relative to the past decade, and can offer meaningful income, yield protection and relatively attractive valuations at present.

Of note as well in the chart above is the tax-equivalent yield that municipal fixed income can provide to top-income tax bracket earners relative to US treasuries.

On the bottom right, we show state rainy day fund balances since 1988, which have increased meaningfully as a result of fiscal transfers from the Federal Government during the pandemic and strong revenue growth. These two charts underscore the attractiveness of municipals from a fundamental perspective, while the left-hand chart highlights the potential yield pick-up in municipals for investors comfortable with increasing duration. In this situation, municipal bonds may be appropriate opportunity for capital-on-the-side that is willing to take a longer-term time horizon and desire an income-focused return.

As always, our client’s individual portfolio allocation are tailored to their specific situations, and we are always evaluating their needs as it relates to their long-term goals.

Our job is to help you stay confident and focused on your long-term financial goals, and, help you understand how to adjust when your individual situation changes. The more you keep us informed of your life as it evolves, the better equipped we are to provide the personal solutions that help you go further, faster.